Risk Management

Tax Implications of Options Trading

A high-level educational overview of options tax topics, recordkeeping, holding periods, wash sales, and why traders should consult a tax professional.

Tax Disclaimer

This article is not tax advice. Tax laws differ by jurisdiction and can change over time. Always consult a qualified tax professional regarding your specific situation.

Overview

Options taxes can become complicated quickly.

Unlike simple stock investing, options trading may involve:

- Multiple contract types.

- Assignment and exercise.

- Rolling positions.

- Spreads.

- Short-term vs long-term holding periods.

- Wash sale rules.

- Adjusted stock basis.

- Index option treatment.

- Trader tax status considerations.

Two trades with similar profit may produce very different tax outcomes depending on:

- Contract structure.

- Holding period.

- Assignment status.

- Jurisdiction.

Many beginners focus entirely on:

- Premium collected.

- Profit/loss.

- Win rate.

But professionals also focus on:

- After-tax outcomes.

- Reporting complexity.

- Recordkeeping quality.

- Realized vs unrealized gains.

This guide provides a high-level educational overview of common tax concepts related to options trading.

It is not tax advice and should not replace professional guidance.

Why Options Taxes Become Complex

Options can interact with stock positions in multiple ways.

For example:

| Situation | Possible Tax Impact |

|---|---|

| Closing a call | Capital gain/loss |

| Exercising a call | Adjusted stock basis |

| Covered call assignment | Affects stock sale reporting |

| Rolling a position | Multiple taxable events |

| Spreads | Multi-leg reporting complexity |

| Index options | Different tax treatment in some jurisdictions |

The complexity often increases when traders:

- Roll positions repeatedly.

- Trade actively.

- Combine stock and options.

- Hold positions across year-end.

High-Level Tax Concepts

1. Capital Gains and Losses

Closing an option position may create:

- Realized gains.

- Realized losses.

Depending on holding period and jurisdiction, those gains may be:

- Short-term.

- Long-term.

- Treated differently under special rules.

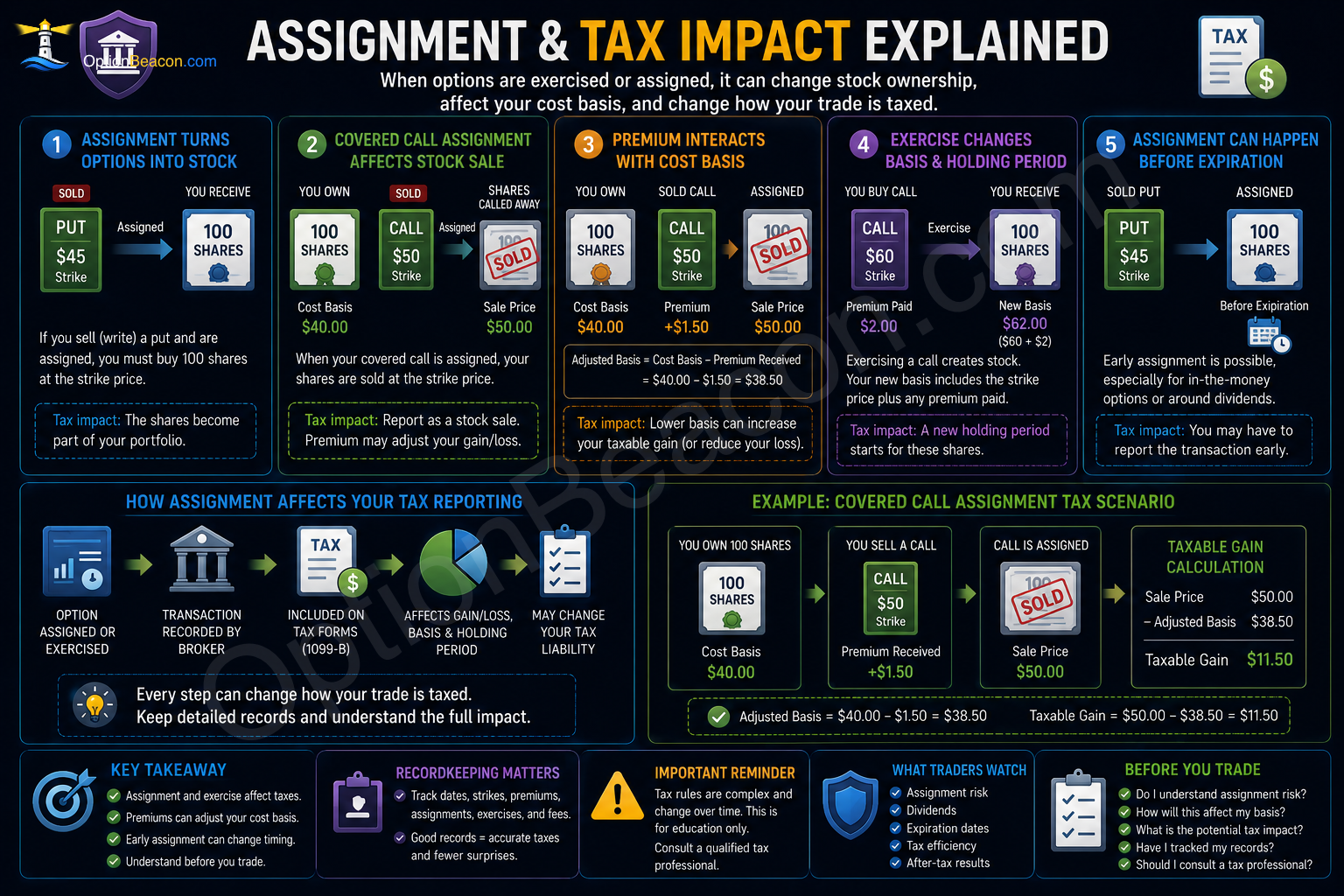

2. Exercise and Assignment

Exercising or being assigned can change:

- Stock cost basis.

- Holding period calculations.

- Realized proceeds.

This surprises many beginners.

The option premium may not always remain isolated from the stock transaction.

3. Holding Periods

Holding period may affect tax treatment.

In many jurisdictions:

| Holding Type | Possible Treatment |

|---|---|

| Short-term | Higher ordinary rates |

| Long-term | Different preferential rates |

But options holding periods may behave differently than stock ownership.

Certain adjustments or assignments may reset timing calculations.

4. Wash Sale Rules

Wash sale rules may apply when:

- Closing positions at a loss.

- Reopening similar positions quickly.

This may:

- Defer losses.

- Adjust basis.

- Complicate reporting.

Wash sale treatment can become especially confusing with:

- Rolling options.

- Similar strikes.

- Multiple expirations.

- Stock and option combinations.

5. Index vs Equity Options

Some jurisdictions treat certain index options differently than equity options.

In the United States, some broad-based index options may receive special tax treatment under specific IRS rules.

But:

- Rules vary significantly by product and jurisdiction.

Never assume all contracts are treated identically.

How Rolling Can Affect Taxes

Rolling usually creates:

1. One closing transaction. 2. One new opening transaction.

That means a roll may:

- Realize gains/losses.

- Create new holding periods.

- Affect wash sale calculations.

- Change adjusted basis.

Many beginners mistakenly think:

- A roll delays taxes.

But rolling is typically a new trade sequence, not a tax reset button.

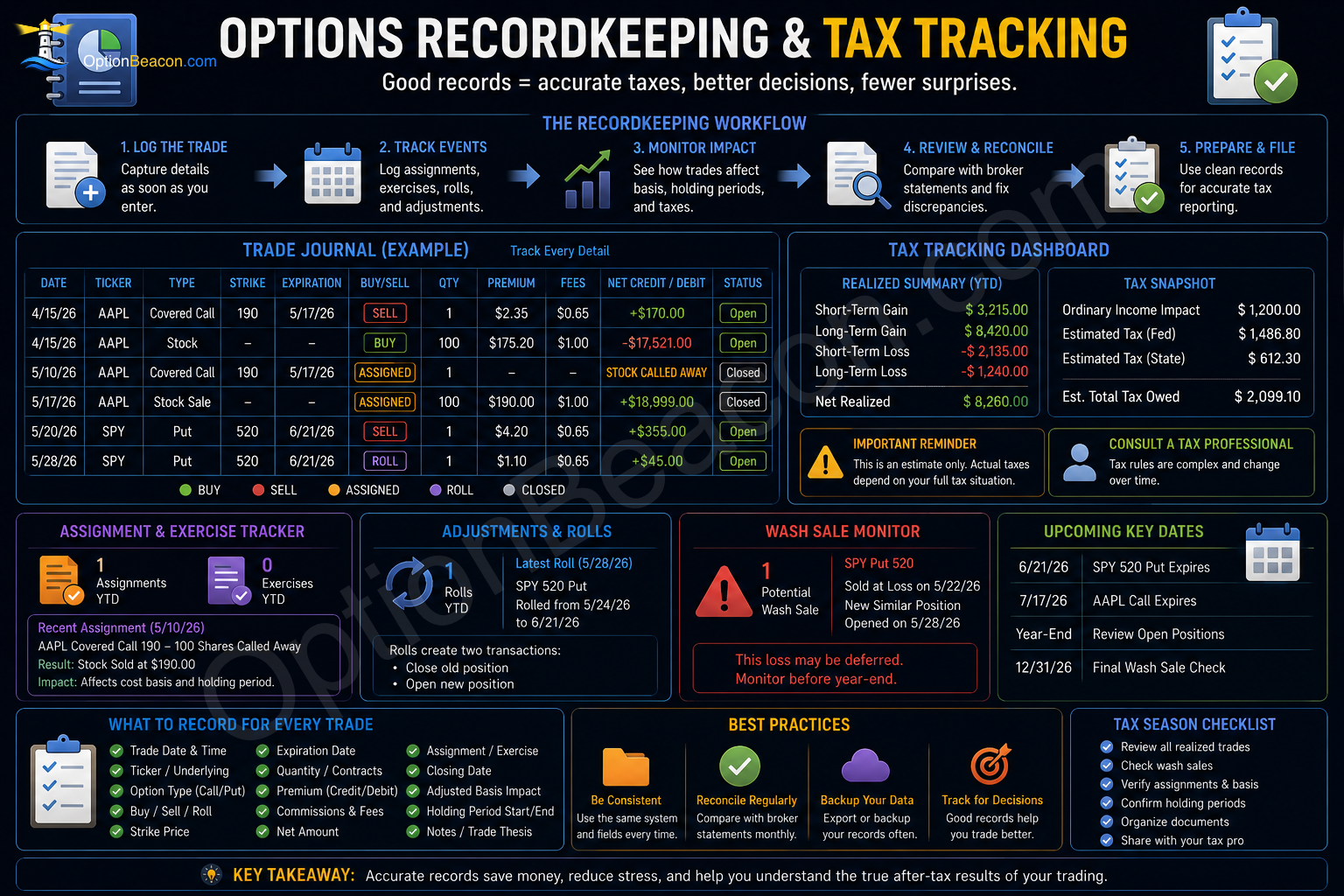

Recordkeeping Matters

Good records become extremely important with options trading.

Professionals usually track:

- Entry date.

- Expiration.

- Strike.

- Premium paid/received.

- Assignment events.

- Exercise events.

- Rolls.

- Commissions and fees.

- Realized P/L.

- Adjusted basis.

Without strong records:

- Reporting errors become more likely.

- Wash sale tracking becomes harder.

- Year-end reconciliation becomes stressful.

Real Example

A trader sells a covered call:

- 100 shares owned.

The call is later assigned.

Possible reporting implications may include:

- Stock sale proceeds.

- Adjusted basis.

- Premium integration.

- Holding period considerations.

This may differ from simply:

- Treating premium as standalone income.

Examples are simplified so the mechanics are easier to see. Real trades also include commissions, fees, taxes, assignment risk, volatility changes, and jurisdiction-specific rules.

Professional Trader Lens

Professionals usually approach taxes proactively instead of reactively.

They often:

- Maintain organized trade records.

- Review realized gains throughout the year.

- Monitor wash sale exposure.

- Evaluate after-tax outcomes.

- Coordinate with tax professionals.

Professional traders understand:

- Gross profit is not the same as net after-tax profit.

For U.S. traders, IRS Publication 550 and broker tax forms may be useful educational starting points, but they are not substitutes for individualized professional advice.

Common Tax Areas Traders Often Miss

Assignment Effects

Assignment can alter stock basis calculations.

Rolling Complexity

Multiple rolls can create chains of taxable events.

Multi-Leg Spreads

Spreads may involve:

- Separate legs.

- Different expirations.

- Different holding periods.

Year-End Position Timing

Positions held into year-end may affect realized vs unrealized reporting.

Cross-Platform Reporting

Using multiple brokers can complicate reconciliation.

Risks and Tradeoffs

Tax Rules Can Change

Regulations evolve over time.

Broker Reporting May Not Capture Everything

Broker statements may not fully reflect nuanced planning situations.

Complex Strategies Increase Reporting Difficulty

More adjustments usually mean more reporting complexity.

Active Trading Creates More Administrative Burden

Frequent trading increases:

- Recordkeeping requirements.

- Reconciliation work.

- Tax preparation complexity.

Emotional Decisions Can Create Tax Problems

Late-year panic adjustments sometimes worsen reporting outcomes.

Common Mistakes

Ignoring Taxes Until Year-End

Many traders wait too long to organize records.

Assuming Every Option Is Taxed the Same

Contract type and structure matter.

Failing to Track Rolls

Rolling can create complex chains of transactions.

Ignoring Wash Sale Risk

Repeated similar trades may trigger deferred losses.

Confusing Realized and Unrealized P/L

Open positions usually behave differently than closed trades for reporting purposes.

Most beginner mistakes come from focusing only on premium instead of total exposure, assignment interaction, and after-tax outcomes.

Practical Recordkeeping Checklist

Track:

- Ticker.

- Strike.

- Expiration.

- Entry/exit date.

- Premium paid/received.

- Assignment events.

- Exercise events.

- Rolls.

- Commissions.

- Adjusted basis changes.

- Realized P/L.

- Broker confirmations.

Good organization early prevents major stress later.

Simple Risk Framework

Before trading actively, ask:

1. How will I track trades? 2. Do I understand assignment implications? 3. Am I rolling positions frequently? 4. Do I understand wash sale basics? 5. Do I know my realized gains/losses? 6. Should I speak with a tax professional?

If those answers are unclear:

- Your reporting process may not be ready for active options trading.

Related Guides

Continue learning:

- Risks of Options Trading

- Rolling an Option: When and Why

- Covered Calls Explained

- Cash-Secured Puts Explained

- Options Expiration and Time Decay

Key Takeaways

- Options taxes can become complex quickly.

- Assignment and exercise may affect stock basis.

- Rolling usually creates new taxable transactions.

- Wash sale rules may complicate reporting.

- Recordkeeping is critical.

- Index and equity options may differ.

- Broker statements may not capture every nuance.

- Professional tax guidance is often worthwhile.

FAQ

Is this tax advice?

No. This article is educational only and is not tax advice. Consult a qualified tax professional regarding your specific situation.

Are index options taxed differently?

Some index products may receive different treatment depending on jurisdiction and contract structure.

Why are rolls important for taxes?

Because rolling typically involves: - Closing one trade. - Opening another. - Realizing gains or losses.

What records should I keep?

Track: - Dates. - Strikes. - Expirations. - Premiums. - Assignments. - Exercises. - Rolls. - Commissions. - Realized P/L.

Can assignment affect stock taxes?

Yes. Assignment may alter: - Basis. - Proceeds. - Holding periods.

Why do active traders use journals?

Because organized records help with: - Tax reporting. - Performance review. - Risk management. - Error detection. ## Educational Disclaimer OptionBeacon provides educational content only and does not provide financial, investment, or trading advice.