Options Basics

Options Expiration and Time Decay

Understand what happens as options approach expiration and why time decay matters for buyers and sellers.

Overview

Expiration is the deadline of an option contract.

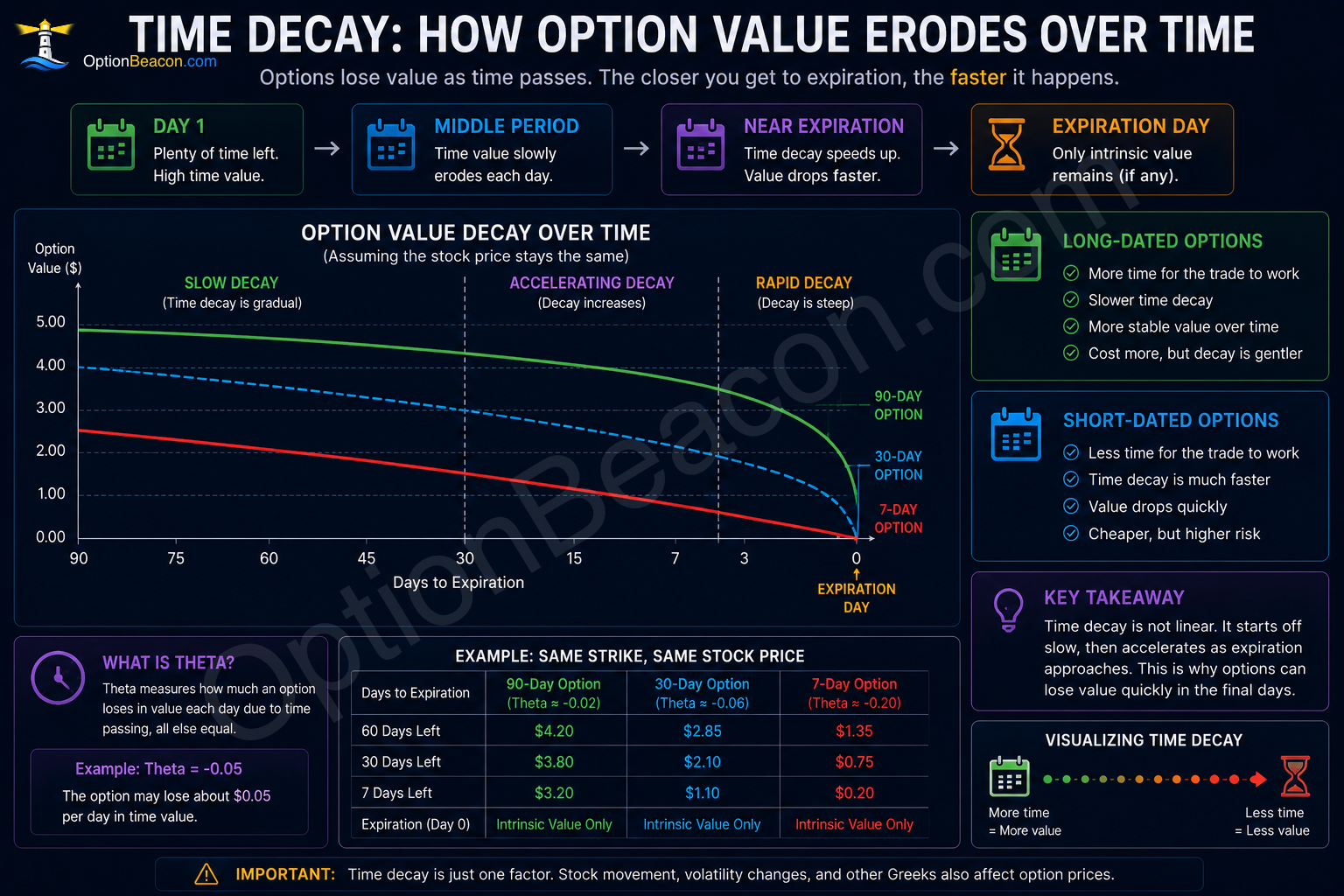

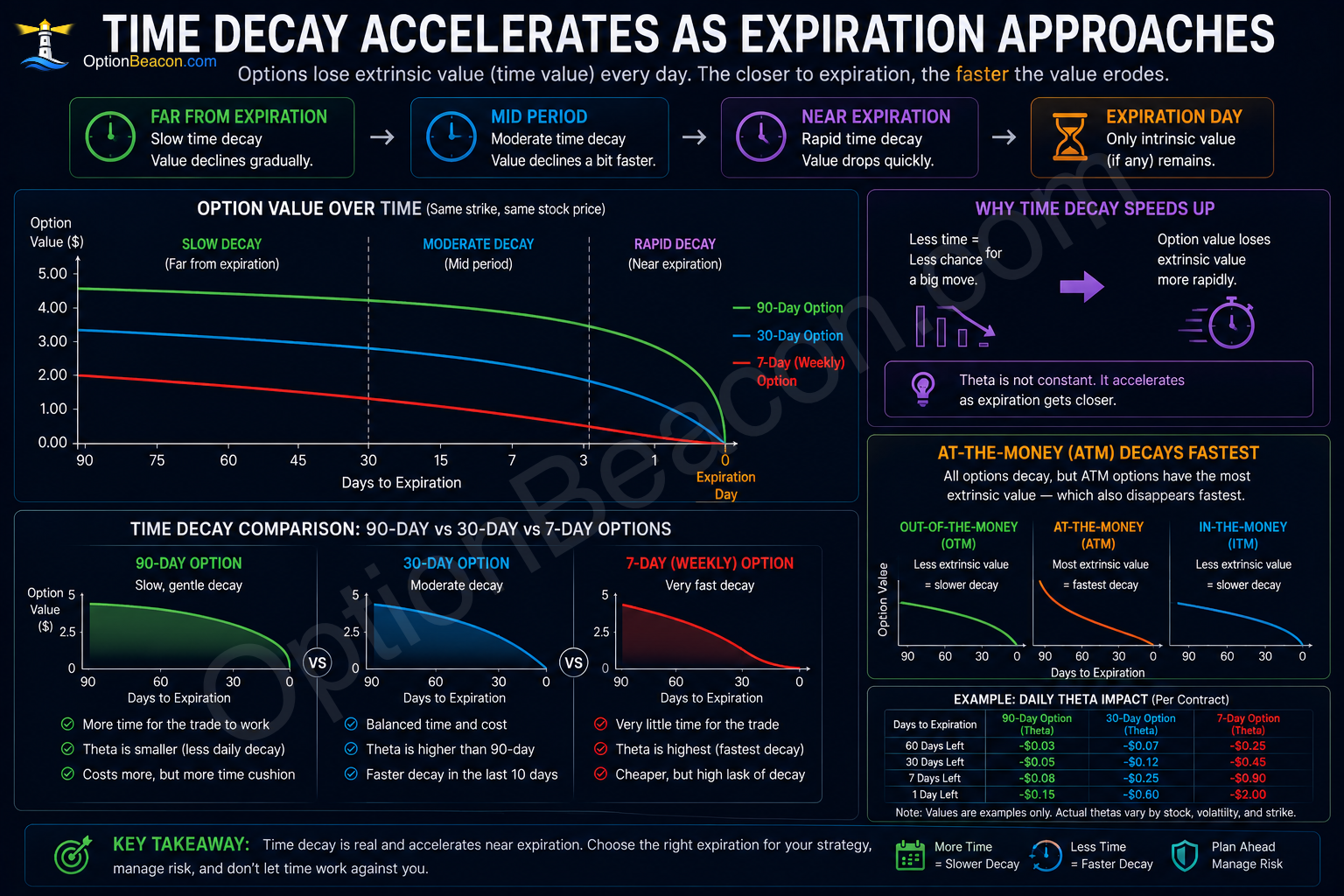

Time decay is the gradual erosion of an option's extrinsic value as that deadline approaches.

Every option contract eventually reaches expiration day.

As time disappears, the probability of a large favorable move also decreases.

This is why options lose value over time even when the stock barely moves.

This guide explains the idea in practical terms. It is written for education, not as a trade recommendation. Before using any options strategy, understand the contract, the maximum realistic loss, the expiration date, liquidity, and what could happen if the position is assigned or exercised.

Simple Explanation

Options are wasting assets.

Unlike shares of stock, options have a limited lifespan.

Every day that passes removes part of the contract's remaining opportunity.

This loss of time value is called theta decay.

The closer expiration gets:

- The faster time decay often becomes.

- The more sensitive options may become.

- The more rapidly exposure can change.

What Is Expiration?

Every option contract has:

- A strike price.

- An expiration date.

Expiration is the final day the contract exists.

After expiration:

- The option may expire worthless.

- The option may retain intrinsic value.

- Exercise or assignment may occur.

The expiration date dramatically affects:

- Premium.

- Probability.

- Gamma exposure.

- Theta decay.

- Assignment risk.

Intrinsic vs Extrinsic Value

Options contain two major components:

| Value Type | Meaning |

|---|---|

| Intrinsic Value | Real in-the-money value |

| Extrinsic Value | Time value and volatility value |

Time decay mainly affects extrinsic value.

As expiration approaches, extrinsic value shrinks.

At expiration:

- Extrinsic value becomes zero.

Theta: The Time Decay Greek

Theta estimates how much value an option may lose from one day passing, all else equal.

Example:

| Theta | Estimated Daily Decay |

|---|

A long option position with:

- Theta = -0.05.

May lose roughly:

- $5 per contract per day.

On a standard 100-share contract.

Why Theta Accelerates

Time decay is not linear.

Theta often accelerates:

- Near expiration.

- In at-the-money contracts.

- During low volatility environments.

This means options may lose value very slowly at first and then much faster near expiration.

Weekly vs Longer-Dated Options

Short-dated contracts and long-dated contracts behave differently.

Weekly Options

Weekly options often:

- Decay faster.

- Have higher gamma risk.

- React aggressively to movement.

- Require more precise timing.

Longer-Dated Options

Longer-dated options often:

- Cost more.

- Decay slower.

- Provide more flexibility.

- Carry higher vega exposure.

A one-week contract is not simply a cheaper version of a three-month contract.

It is a completely different risk structure.

Real Example

A trader buys a:

- 30-day call option for $3.00.

If:

- The stock does not move.

- Implied volatility does not increase.

The option may still lose value simply because there is less time remaining for a favorable move.

As expiration approaches:

- Theta decay accelerates.

- The option may lose premium faster.

- Probability changes rapidly.

Examples are simplified so the mechanics are easier to see. Real trades also include commissions, fees, taxes, changing implied volatility, early assignment risk, and execution quality.

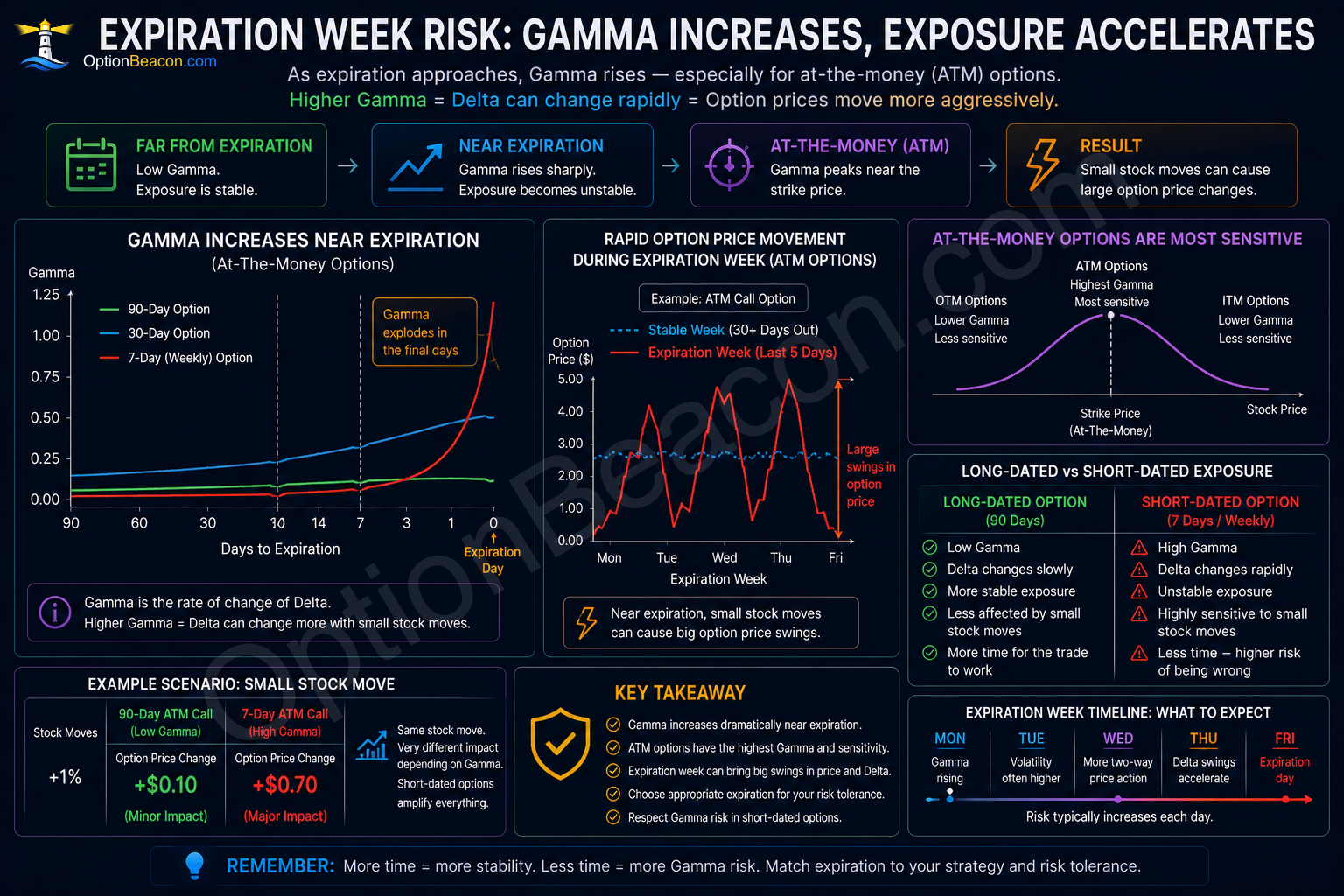

Expiration and Gamma Risk

Gamma risk often increases near expiration.

This means delta exposure can change very quickly.

Short-dated options near the strike price may experience:

- Large swings in exposure.

- Aggressive premium changes.

- Rapidly changing probability.

This is why expiration week can feel dramatically different from earlier periods.

What Happens At Expiration?

At expiration, the option either:

- Expires worthless.

- Retains intrinsic value.

- Gets exercised or assigned.

Out-Of-The-Money Options

OTM contracts usually expire worthless.

Example:

| Stock Price | Call Strike |

|---|---|

| $100 | $105 Call |

If the stock remains below:

- $105.

The call may expire worthless.

In-The-Money Options

ITM contracts may:

- Retain intrinsic value.

- Be exercised automatically.

- Create assignment risk for sellers.

Assignment Risk Near Expiration

Assignment risk becomes increasingly important for:

- Short calls.

- Short puts.

- Covered calls.

- Spreads.

Especially when:

- Contracts are in the money.

- Expiration approaches.

- Dividends are involved.

Many traders reduce or close exposure before expiration to avoid unexpected assignment.

Professional Trader Lens

Professionals match expiration to the trade thesis.

They ask:

- How long should this idea realistically take?

- Is there enough time for the thesis to play out?

- Is the premium justified relative to time remaining?

- Am I taking too much gamma risk?

- Does the position still make sense if volatility changes?

Professional traders understand:

- Time is part of the trade structure.

A professional process usually starts with:

- The underlying stock.

- Implied volatility.

- Strategy selection.

- Expiration selection.

- Position size.

The option contract is the expression of the idea, not the idea itself.

Risks and Tradeoffs

- Short-dated options can lose premium quickly.

- Gamma risk increases near expiration.

- Assignment risk becomes more important near expiration.

- Weekly options may require precise timing.

- Long-dated contracts cost more and carry different volatility exposure.

Risk should be reviewed before entry and again after the trade changes.

Options positions can evolve quickly because delta, gamma, theta, and vega are not static.

A position that looked conservative at entry can become aggressive after a large move or as expiration approaches.

Common Mistakes

Buying options with too little time

Beginners often underestimate how long market movement can take.

Ignoring theta decay

Even correct directional ideas can lose money because of time decay.

Holding short options into expiration without a plan

Assignment and gamma risk may increase rapidly.

Trading weekly options too aggressively

Short-dated contracts can behave very differently from longer-dated options.

Ignoring earnings and event timing

Major events can dramatically affect:

- Implied volatility.

- Theta behavior.

- Expiration risk.

Most beginner mistakes come from focusing on premium instead of total exposure.

Premium is visible immediately, but the obligation, drawdown, opportunity cost, and assignment scenario matter just as much.

Practical Checklist

Before selecting expiration:

- Does the contract provide enough time for the thesis?

- Have you considered theta decay?

- Are earnings or major events approaching?

- Do you understand assignment exposure?

- Is gamma risk acceptable?

- Does the expiration match your strategy structure?

- Is the position small enough to manage responsibly?

Choosing the Right Expiration

There is no perfect expiration.

The best expiration depends on:

- Market thesis.

- Timing expectations.

- Volatility.

- Strategy structure.

- Risk tolerance.

Good expiration selection balances:

- Time.

- Probability.

- Premium.

- Gamma exposure.

- Theta decay.

Related Beginner Guides

Continue learning:

- The Greeks: Delta, Gamma, Theta, and Vega

- Understanding Implied Volatility

- How to Read an Options Chain

- How to Choose the Right Strike Price

- Risks of Options Trading

Key Takeaways

- Every option contract has an expiration date.

- Time decay erodes extrinsic value.

- Theta often accelerates near expiration.

- Weekly options behave differently from long-dated contracts.

- Gamma risk increases near expiration.

- Expiration selection changes risk structure.

- Time itself is part of the trade.

FAQ

What happens at expiration?

The option either retains intrinsic value or expires worthless depending on moneyness and exercise rules.

Is theta always bad?

Theta hurts long options but can help short option positions, assuming other risks are managed.

Should I hold options until expiration?

Many traders close or adjust before expiration to reduce assignment and gamma risk.

Why do options lose value over time?

As expiration approaches, there is less opportunity for a favorable move.

Why are weekly options risky?

Weekly contracts often have faster theta decay and higher gamma sensitivity.

Can an option lose value even if the stock does not move?

Yes. Time decay alone may reduce option value.