Options Basics

The Greeks: Delta, Gamma, Theta, and Vega

A beginner-friendly guide to the option Greeks and how they help explain price changes in options contracts.

Overview

The Greeks estimate how an option price may respond to:

- Stock movement.

- Time passing.

- Implied volatility.

- Changes in exposure.

They are not predictions.

They are risk measurements.

The Greeks help traders understand why an option changes value even when the stock barely moves.

This guide explains the idea in practical terms. It is written for education, not as a trade recommendation. Before using any options strategy, understand the contract, the maximum realistic loss, the expiration date, liquidity, and what could happen if the position is assigned or exercised.

Simple Explanation

The Greeks are tools that estimate how sensitive an option is to different forces.

Think of them as:

| Greek | What It Measures |

|---|---|

| Delta | Stock price movement |

| Gamma | Delta acceleration |

| Theta | Time decay |

| Vega | Implied volatility changes |

The Greeks help answer questions like:

- How much could this option move?

- How fast is time decay happening?

- How sensitive is this contract to volatility?

- How quickly can exposure change?

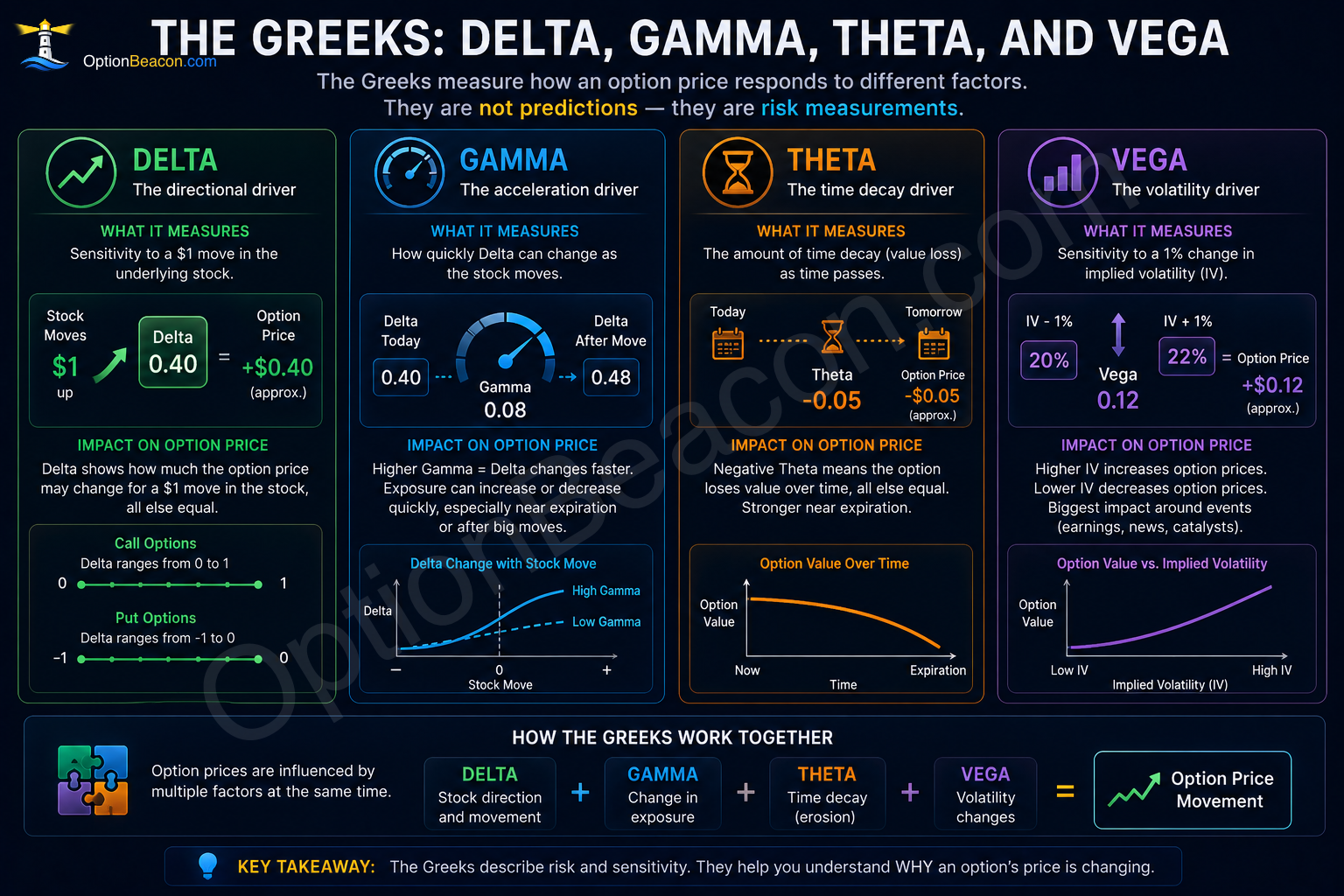

Delta

Delta estimates how much an option price may change for a $1 move in the underlying stock.

Example:

A call with:

- 0.40 delta.

May gain approximately:

- $0.40.

If the stock rises by:

- $1.

All else equal.

What Delta Helps Explain

- Directional exposure.

- Sensitivity to stock movement.

- Approximate responsiveness of the contract.

Higher delta options generally:

- Cost more.

- Move more like stock.

- Contain more intrinsic value.

Lower delta options generally:

- Cost less.

- Require larger movement.

- Are more speculative.

Common Beginner Interpretation

Many beginners think delta predicts profit.

It does not.

Delta is dynamic and changes constantly.

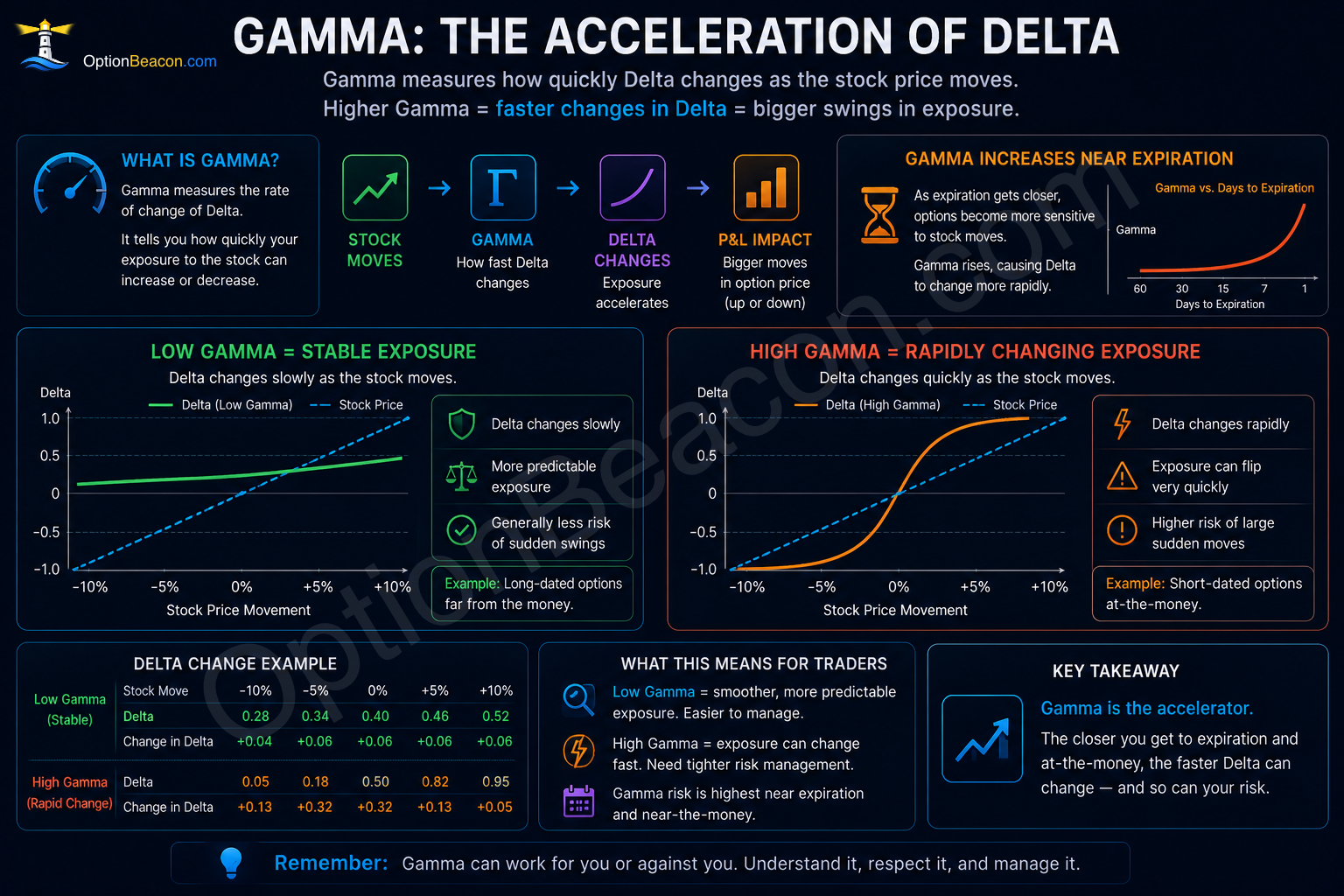

Gamma

Gamma estimates how quickly delta can change.

It measures acceleration.

Gamma becomes especially important:

- Near expiration.

- During large stock movement.

- Around major events.

High gamma means exposure can change very quickly.

Why Gamma Matters

An option with:

- 0.40 delta.

May not stay at:

- 0.40.

If the stock moves aggressively, delta itself may increase or decrease rapidly.

This can create:

- Larger gains.

- Larger losses.

- Rapidly changing exposure.

Theta

Theta estimates time decay.

It measures how much value an option may lose as time passes.

All else equal:

- Time passing hurts long options.

Theta is often strongest:

- Near expiration.

- For out-of-the-money contracts.

- During low movement periods.

Why Theta Matters

An option can lose value even when:

- The stock barely moves.

- The direction is correct.

- Implied volatility stays stable.

Time itself has value.

As expiration approaches, that time value shrinks.

Common Beginner Mistake

Many beginners focus only on direction while ignoring time decay.

This is one of the most common reasons long options lose money.

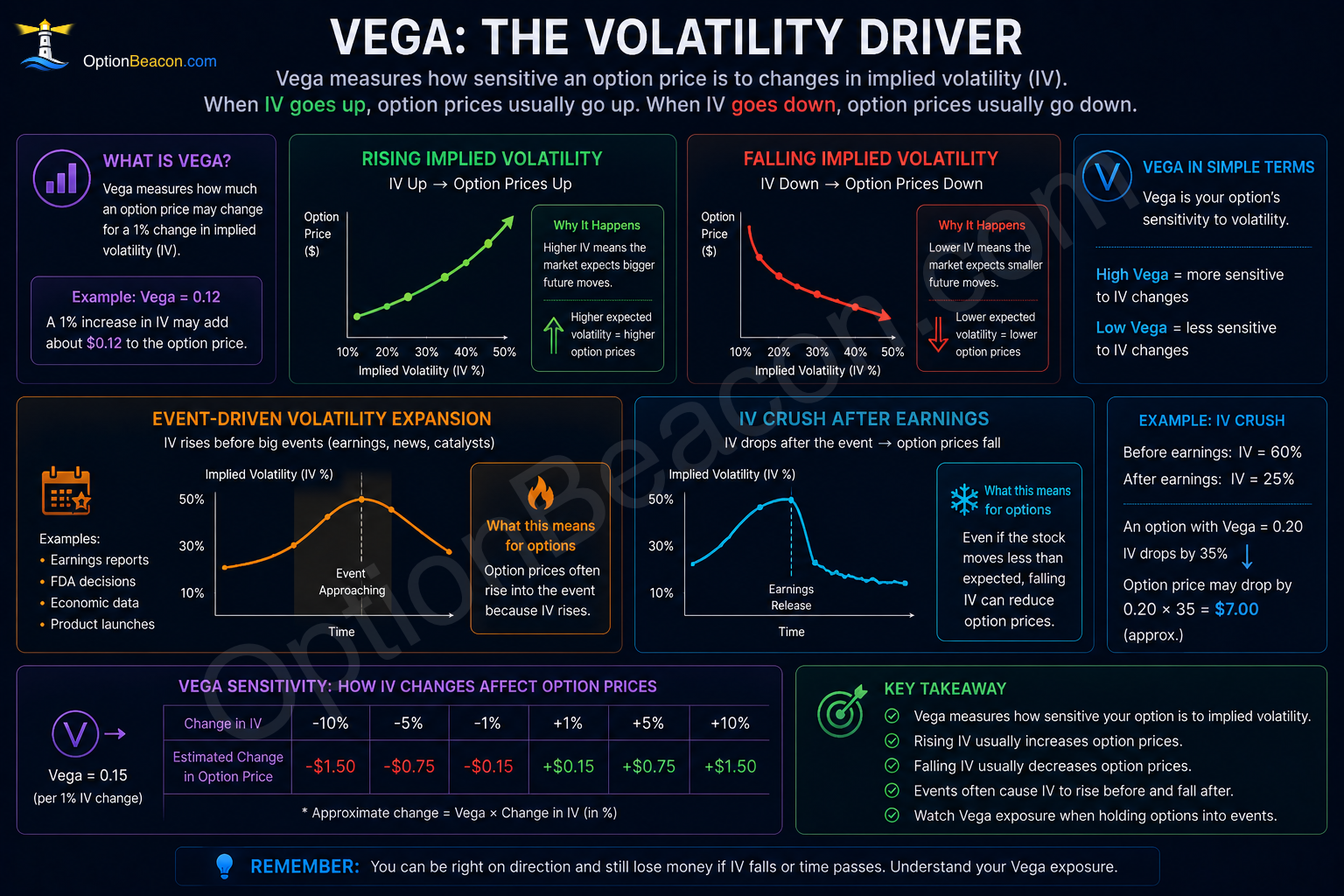

Vega

Vega estimates sensitivity to implied volatility.

When implied volatility rises:

- Option premiums often increase.

When implied volatility falls:

- Option premiums often decrease.

Vega exposure becomes especially important:

- Before earnings.

- During market uncertainty.

- Around major news events.

Why Vega Matters

An option buyer may correctly predict stock direction and still lose money if:

- Implied volatility collapses.

- Time decay offsets movement.

- The move is smaller than expected.

This is why understanding implied volatility matters.

How the Greeks Work Together

The Greeks are connected.

They do not operate independently.

Example:

- Delta may increase because of gamma.

- Theta decay may accelerate near expiration.

- Vega exposure may dominate during earnings.

- Multiple Greeks may affect pricing at the same time.

This is why options can behave differently than beginners expect.

Real Example

Suppose a call option has:

| Greek | Value |

|---|---|

| Delta | 0.40 |

| Theta | -0.05 |

| Vega | 0.12 |

If the stock rises:

- $1.

The option may gain approximately:

- $0.40.

From delta exposure.

But if:

- Implied volatility falls.

- Time passes.

- Gamma changes exposure.

The actual result may differ significantly.

Examples are simplified so the mechanics are easier to see. Real trades also include commissions, fees, taxes, changing implied volatility, early assignment risk, and execution quality.

Professional Trader Lens

Professionals use Greeks to understand exposure before entering a trade and to monitor how exposure changes after entry.

They often ask:

- What is driving the option price?

- Is this mostly delta exposure or volatility exposure?

- How much theta decay am I accepting?

- How quickly can exposure change?

Professional traders understand that:

- Greeks describe risk exposure, not certainty.

A professional process usually starts with:

- The underlying stock.

- Implied volatility.

- Strategy selection.

- Strike selection.

- Position size.

The option contract is the expression of the idea, not the idea itself.

Risks and Tradeoffs

- Greeks change constantly.

- Gamma can accelerate near expiration.

- High theta can rapidly decay long options.

- High vega exposure can hurt after events such as earnings.

- Multiple Greeks can affect the same position simultaneously.

Risk should be reviewed before entry and again after the trade changes.

Options positions can evolve quickly because delta, gamma, theta, and vega are not static.

A position that looked conservative at entry can become aggressive after a large move or as expiration approaches.

Common Mistakes

Treating Greeks as guaranteed forecasts

Greeks are estimates, not promises.

Looking only at delta

Delta matters, but theta and vega may dominate in certain environments.

Ignoring time decay

Theta becomes increasingly important near expiration.

Selling options near expiration without respecting gamma risk

Exposure can change very quickly in short-dated contracts.

Ignoring implied volatility

Vega exposure can dramatically affect pricing around earnings and major events.

Most beginner mistakes come from focusing on premium instead of total exposure.

Premium is visible immediately, but the obligation, drawdown, opportunity cost, and assignment scenario matter just as much.

Practical Checklist

Before entering an options trade:

- Do you understand the main Greek exposure?

- Is the position mostly directional or volatility-driven?

- How much theta decay are you accepting?

- Could gamma accelerate exposure near expiration?

- Are earnings or major events approaching?

- Does the position size match your risk tolerance?

Which Greek Should Beginners Learn First?

Most beginners should start with:

- Delta.

- Theta.

- Vega.

- Gamma.

Delta and theta are usually the most intuitive starting points.

Gamma and vega become more important as traders study volatility and short-dated contracts.

Related Beginner Guides

Continue learning:

- Understanding Implied Volatility

- How to Read an Options Chain

- Options Expiration and Time Decay

- How to Choose the Right Strike Price

- Risks of Options Trading

Key Takeaways

- Greeks estimate option sensitivity to different forces.

- Delta measures stock price exposure.

- Gamma measures how quickly delta changes.

- Theta measures time decay.

- Vega measures implied volatility exposure.

- Greeks change constantly.

- Multiple Greeks can affect the same trade simultaneously.

- Greeks describe exposure, not certainty.

FAQ

Which Greek should beginners learn first?

Delta and theta are usually the most intuitive starting points.

Is delta probability?

Delta is sometimes used as a rough proxy, but it is not the same as true probability.

Do all strategies have Greeks?

Yes. Every option position has Greek exposure, including spreads and covered positions.

Why does theta hurt option buyers?

Long options lose time value as expiration approaches.

Why is gamma dangerous near expiration?

Exposure can change rapidly, creating larger-than-expected gains or losses.

Why does implied volatility affect options so much?

Implied volatility changes option pricing because it affects expected future movement.