Options Basics

Understanding Implied Volatility

Learn how implied volatility affects option prices and why expensive options can still lose money after a correct directional call.

Overview

Implied volatility reflects the market price of expected movement. It is embedded in option prices and can change quickly.

This guide explains the idea in practical terms. It is written for education, not as a trade recommendation. Before using any options strategy, understand the contract, the maximum realistic loss, the expiration date, liquidity, and what could happen if the position is assigned or exercised.

Implied Volatility — Simple Explanation

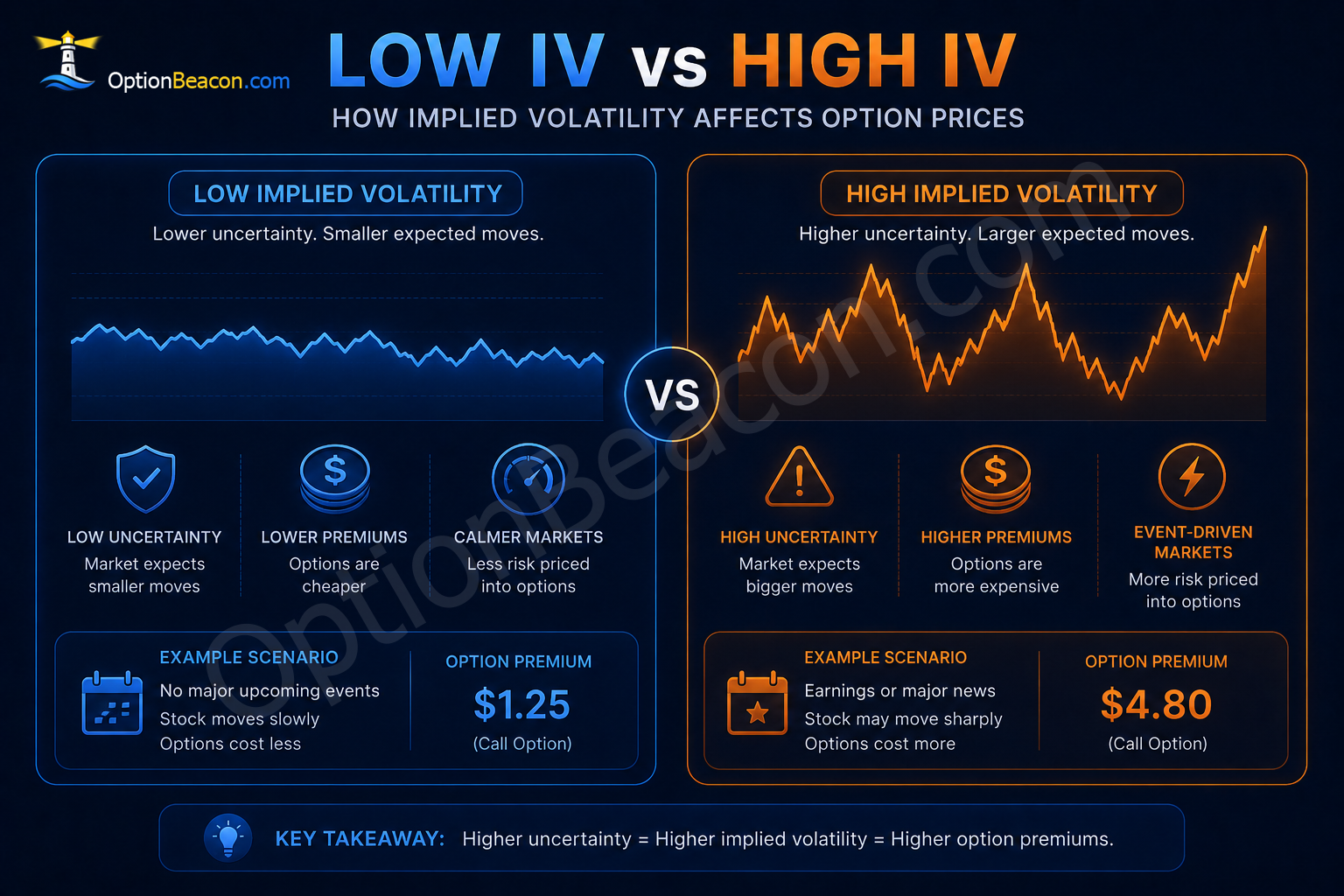

Implied volatility reflects how much movement the market expects in the future.

Higher implied volatility usually means:

- More uncertainty.

- Larger expected price swings.

- More expensive options.

Lower implied volatility usually means:

- Calmer expectations.

- Smaller expected moves.

- Cheaper options.

Implied volatility does not predict whether a stock will go up or down. It reflects expected movement magnitude.

How It Works

- Higher implied volatility generally means higher option premiums.

- Lower implied volatility generally means cheaper premiums.

- Vega estimates sensitivity to implied volatility.

- Event-driven volatility often falls after the event passes.

The important professional habit is to connect the structure to a specific thesis. A trader should be able to explain:

- What they expect to happen.

- What would prove the idea wrong.

- How much capital is at risk if the market behaves unexpectedly.

A professional process usually starts with the underlying first, then volatility, then strategy selection, then position size. The option contract is the expression of the idea, not the idea itself.

Why Options Become More Expensive

When implied volatility rises, option premiums often increase because the market expects larger future movement.

This commonly happens before:

- Earnings reports.

- Major economic announcements.

- FDA decisions.

- Product launches.

- Unexpected news events.

Higher implied volatility increases uncertainty, and uncertainty often increases option pricing.

Does Implied Volatility Predict Direction?

No.

Implied volatility reflects expected movement size, not direction.

A stock with high implied volatility may move sharply:

- Higher.

- Lower.

- Or both within a short period.

Many beginners incorrectly assume high implied volatility means bullish sentiment. In reality, it usually reflects uncertainty and larger expected movement.

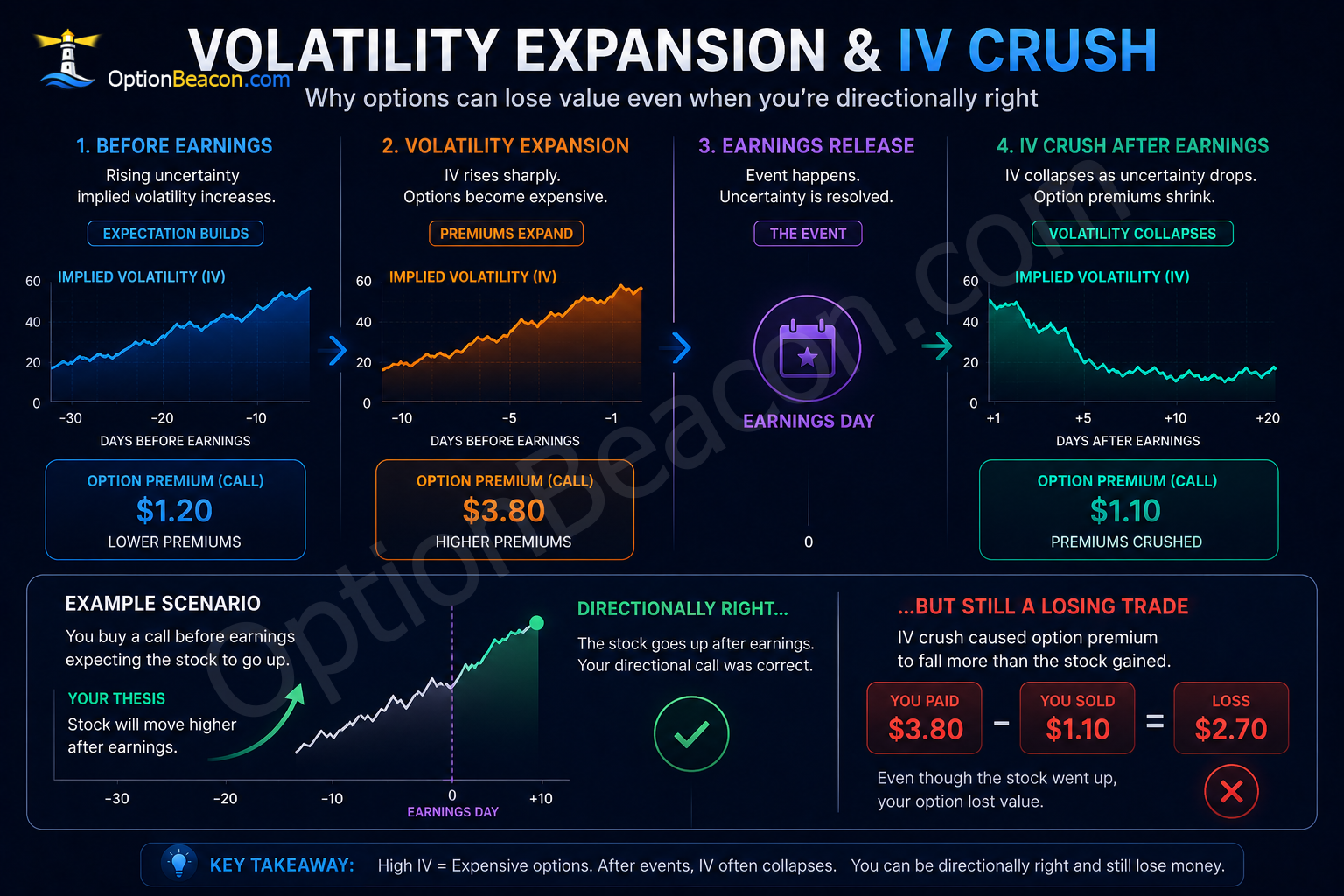

Real Example

Before earnings, options may price in a large expected move. After earnings, implied volatility can drop quickly.

A call buyer may be directionally right but still lose money if:

- The stock move is smaller than expected.

- Implied volatility falls sharply after the event.

- Time decay offsets the directional gain.

Examples are simplified so the mechanics are easier to see. Real trades also include commissions, fees, taxes, changing implied volatility, early assignment risk, and execution quality.

What Is IV Crush?

IV crush is a rapid drop in implied volatility after a major anticipated event.

This often happens after:

- Earnings reports.

- Fed announcements.

- Important company news.

- Major market events.

Before the event, options may become expensive because the market expects large movement.

After the event passes, uncertainty often decreases quickly, causing option premiums to shrink.

This can hurt long option buyers even if the stock moves in the expected direction.

High IV vs Low IV

| Low Implied Volatility | High Implied Volatility |

|---|---|

| Lower option premiums | Higher option premiums |

| Smaller expected movement | Larger expected movement |

| Lower uncertainty | Higher uncertainty |

| Often calmer markets | Often event-driven markets |

| Lower Vega exposure | Higher Vega exposure |

Professional Trader Lens

Professionals compare implied volatility with:

- Realized movement.

- Event timing.

- Historical volatility.

- Liquidity.

- Overall market conditions.

They avoid assuming high premium automatically means easy income.

Professional traders also understand that volatility changes constantly. A strategy that looks conservative in one volatility environment may behave very differently in another.

Risks and Tradeoffs

- Volatility crush can hurt long options.

- Short volatility trades can lose heavily if movement exceeds expectations.

- Implied volatility does not predict direction.

- High implied volatility can increase both opportunity and risk.

Risk should be reviewed before entry and again after the trade changes. Options positions can evolve quickly because delta, gamma, theta, and vega are not static.

A position that looked conservative at entry can become aggressive after a large move or as expiration approaches.

Common Mistakes

Buying options before events without checking implied volatility

Many beginners buy options before earnings without realizing premiums may already price in large expected movement.

Selling options because premium looks high without understanding why

High premium often exists because risk is elevated.

Ignoring Vega in longer-dated options

Longer-dated contracts can react strongly to changes in implied volatility.

Assuming implied volatility predicts direction

High implied volatility reflects expected movement magnitude, not bullish or bearish direction.

Focusing only on premium

Most beginner mistakes come from focusing on premium instead of total exposure.

Premium is visible immediately, but the obligation, drawdown, opportunity cost, and assignment scenario matter just as much.

Practical Checklist

Before entering an options trade involving volatility exposure:

- Can you explain the strategy without looking at the order ticket?

- Do you know the maximum planned loss and the realistic worst-case scenario?

- Have you checked bid-ask spread, open interest, and upcoming events?

- Do you understand how implied volatility could change after the event?

- Do you know what you will do if the trade moves against you?

- Is the position small enough that you can follow your plan?

Related Beginner Guides

Continue learning:

- What Is an Option?

- Call vs Put Options Explained

- The Greeks: Delta, Gamma, Theta, and Vega

- Options Expiration and Time Decay

- Risks of Options Trading

Key Takeaways

- Implied volatility reflects expected future movement.

- Higher IV usually means more expensive options.

- IV does not predict direction.

- Volatility often rises before major events.

- IV crush can hurt long option buyers.

- Expensive options are not automatically bad trades.

- Risk and volatility should always be evaluated together.

FAQ

What is implied volatility?

Implied volatility reflects the market's expectation of future price movement and is embedded in option pricing.

Does implied volatility affect option prices?

Yes. Higher implied volatility generally increases option premiums, while lower implied volatility often reduces premiums.

Is high implied volatility good?

It depends on the strategy. Higher implied volatility may benefit option sellers collecting larger premiums, but it also signals larger expected movement and increased uncertainty.

What is volatility crush?

A fast drop in implied volatility, often after earnings or another anticipated event.

Does IV predict direction?

No. It relates to expected movement magnitude, not whether the market will move up or down.

Why do options become expensive before earnings?

Before earnings, the market often expects larger movement, which increases implied volatility and option premiums.

Can options lose value after earnings even if the direction was correct?

Yes. If implied volatility drops sharply after earnings, the option can lose value despite a correct directional move.

Is implied volatility the same as historical volatility?

No. Historical volatility measures past movement. Implied volatility reflects future movement expectations embedded in option prices.